Defining Manufacturing Costs vs Production Costs

A cost management system can integrate seamlessly with other business tools such as ERP, accounting software, and supply chain management systems. This allows for streamlined data flow between departments, improving overall efficiency. To give you an idea as to what manufacturing costs are, it’s often helpful to share an example that illustrates the idea. Let’s imagine Acme Manufacturing, a fictitious company that manufactures dog houses. Direct costs impact the operating cash flow section, which reflects cash spent on materials, labor, and production-related expenses. Another commonly used term for manufacturing costs is product costs, which also refer to the costs of manufacturing a product.

Helps in Accurate Pricing

It should also be safe to assume that the more pies made, the greater the number of labor hours experienced (also assuming that direct labor has not been replaced with a greater amount of automation). We assume, in this case, that one of the marketing advantages that the bakery advertises is 100% handmade pastries. For instance, Ford Motor Company has reduced the price of F-150 Lightning, its electric car, by $10,000. The company has been able to do so by consistently working on improving the efficiency of production and lowering manufacturing costs. For that purpose, the company used sensors to collect and analyze the cost of materials in real time to see how to optimize the costs.

What are material costs in manufacturing?

Examples are steel in automobiles, rubber in tires, fabric in clothing, etc. Direct labor refers to the salaries and wages of workers who transform the materials into finished goods. It can be even more critical for small and medium-sized enterprises as they often operate on thinner margins and have less room for error. The frequency of manufacturing cost analysis depends on the nature and scale of the business. However, performing this analysis at least quarterly is advisable to align with financial reporting periods. For businesses experiencing rapid changes, a monthly analysis may be more appropriate.

What are the main components of total manufacturing cost?

The expense recognition principle also applies to manufacturing overhead costs. The manufacturing overhead is an expense of production, even though the company is unable to trace the costs directly to each specific job. For example, the electricity needed to run production equipment typically is not easily traced to a particular product or job, yet it is still a cost of production. As a cost of production, the electricity—one type of manufacturing overhead—becomes a cost of the product and part of inventory costs until the product or job is sold. Fortunately, the accounting system keeps track of the manufacturing overhead, which is then applied to each individual job in the overhead allocation process.

- Utilizing time-tracking software and optimizing shift schedules can help reduce overtime expenses while maintaining efficiency.

- Based on this information, the company’s management can add a markup to determine competitive selling prices for their products.

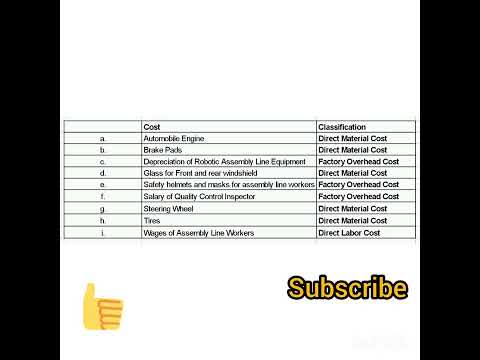

- Manufacturing overhead is any manufacturing cost that is neither direct materials cost nor direct labour cost.

- But they also serve as a means of monitoring labor costs to make sure you’re not overspending your budget.

- Direct labor, as mentioned above, refers to the salaries of production workers.

- Common examples include raw materials, direct labor wages, and production supplies—anything that directly contributes to creating a product or delivering a service.

- ProjectManager is award-winning project management software that tracks manufacturing costs in real time.

Where does the time go?

Common examples are metals like steel, plastic, fabrics used in textiles, and electronics components. These materials constitute a significant portion of the manufacturing budget due to their direct involvement in the product creation. As direct materials, direct labor, and overhead are introduced into the production process, they become part of the work in process inventory value. When the home is completed, the accumulated costs become part of the finished goods inventory value, and when the home is sold, the finished goods value of the home becomes the cost of goods sold.

In cost accounting, the manufacturing process refers to the operations and activities that convert raw materials into finished goods. This process encompasses a range of steps, including material procurement, production, assembly, quality control, and packaging. Lowering production costs without compromising quality is feasible through various strategies such as implementing efficient supply chain management, reducing waste, and optimizing logistics.

Production and manufacturing costs determine supply chain and logistics business performance. Operation success depends on understanding these two cost categories and their differences. In this article, we will look at the differences between manufacturing costs and production costs. Many businesses struggle how to create debit memo in sap to define where one cost set ends and the next begins.

Depreciation is calculated based on equipment lifespan using methods like straight-line or declining balance. Energy-efficient practices can lower utility expenses, while regular maintenance extends equipment life, reducing costs over time. Manufacturing cost analysis is breaking down and studying the various production costs. The objective is to understand the cost structure, temporary accounts identify inefficiencies, and find opportunities for cost optimization.

Direct labor, as mentioned above, refers to the salaries of production workers. Factory overhead refers to costs incurred in production other than direct materials and direct labor. As we defined above, manufacturing overhead costs are all the costs not related to direct labor and direct material costs.

Step-by-Step Guide to Calculate Total Manufacturing Cost

Determining manufacturing costs is important; it helps manufacturers price their products in such a way that they’re competitive but also ensures high net profits for the company. Knowing the manufacturing cost gives manufacturers the ability to meet goals and make sure their production process is at the right level of productivity. Being able to make accurate estimates of your manufacturing costs is critical to a company’s profitability and competitive advantage. Before work hits the production line, one must know how to calculate manufacturing cost.

Cost-based contracts may include a guaranteed maximum, time and materials, or cost reimbursable contract. The training company may charge for the hours worked by instructors in preparation and delivery of the course, plus a fee for the course materials. Manufacturing cost analysis involves understanding components such as direct materials, direct labor, and manufacturing overhead. Understanding the components of manufacturing costs is essential for any business aiming to gain a competitive edge. Typically, costs can international tools and resources be classified into three distinct parts, which are direct materials, direct labor, and manufacturing overhead. Each element influences the total cost structure differently and necessitates a tailored approach for maximizing efficiency.

Proper classification of direct costs is essential for accurate financial statements and tax compliance. Direct costs are included in COGS on income statements, affecting net income and tax liabilities. Misclassifying costs can lead to financial inaccuracies and compliance issues.

Timesheets can help manufacturers streamline their payroll with a secure process that includes locking timesheets once submitted to managers, who can review and route them to payroll. But they also serve as a means of monitoring labor costs to make sure you’re not overspending your budget. Managers can view timesheets to monitor labor costs and get further information by generating a timesheet report. Direct labor costs can fluctuate due to wage increases, overtime payments, or workforce shortages. In industries reliant on skilled labor, retaining employees while managing labor expenses can be a challenge. The raw materials and work-in-progress inventory are considered assets until the final product is sold.

- Using financial management tools helps businesses accurately allocate and monitor direct costs.

- Product costs are costs necessary to manufacture a product, while period costs are non-manufacturing costs that are expensed within an accounting period.

- The terms direct materials and finished goods can be defined by the view of an individual manufacturing company.

- The objective is to identify variances, which are the differences between actual and budgeted costs, and to determine the reasons behind these variances.

- When both administrative and production activities occur in a common building, the production and period costs would be allocated in some predetermined manner.

- For this purpose, she determines the total manufacturing cost per unit and finds out that the cost of manufacturing a chair has gone up by 10% due to the rise in labor and material costs.

Examples include rent and salaried employees not directly involved in production. Effective cost management systems help control expenses, improve efficiency, and boost profitability. Integrating these systems with other business tools ensures smooth operations and better decision-making. For example, if you use 100 units of material that costs $5 each, the total cost for that material is $500. The manufacturing cost is a factor in the total delivery cost or the money a manufacturer spends to make and deliver the product. Managing direct costs effectively requires real-time tracking, automation, and data-driven decision-making.

This requires close coordination with suppliers to ensure materials arrive precisely when needed, improving cash flow and minimizing storage expenses. Bulk purchasing agreements can also provide cost savings, further optimizing the overall cost structure. This hypothetical example is simplified, whereas the actual situation could be much more complex.